Liquidity Crisis at IL&FS – A Closer Look at the Big Picture

Arnab Bhattacharya Download Article

‘Never let a good crisis go to waste’

During September 2018, a series of announcements by the Infrastructure Leasing and Financial Services Ltd (IL&FS) Group, one of the largest infrastructure financing companies in India, revealed that the firm is going through a severe financial distress. Particularly, the public announcements informed the investors that the company had failed to meet its immediate obligations on a Letter of Credit (LC) payment to IDBI Bank, interest payments on Non-Convertible Debentures (NCDs) and other payment obligations with respect to bank loans, short-term deposits and term deposits. These announcements took the market by surprise, and led to a significant disruption in the subsequent months. In this article, we shall attempt to explore a series of recent events that are related to the liquidity distress factors in the Indian NBFC (Non-Banking Financial Company) sector. We shall also discuss some of the major causes and consequences of these events for the Indian capital market investors, infrastructure and real estate companies, government and regulatory agencies and the broader economy in general.

How important are the issues under discussion? – A quick look at the market reaction

Even if you do not generally follow news related to the NBFC sector, the degree of market reaction to the IL&FS crisis might have attracted your attention. So, we begin our analysis by directly examining the market reactions first, before getting to the underlying events that have triggered these intense reactions in the capital market. This serves two important purposes. It will give you an insight into the market perceptions and reactions leading up to this crisis, its root causes and corrective and preventive actions. It will also enable you to see how a crisis may affect not only the corporate sector in general, but also impact your personal finance through its effects on your portfolio investments.

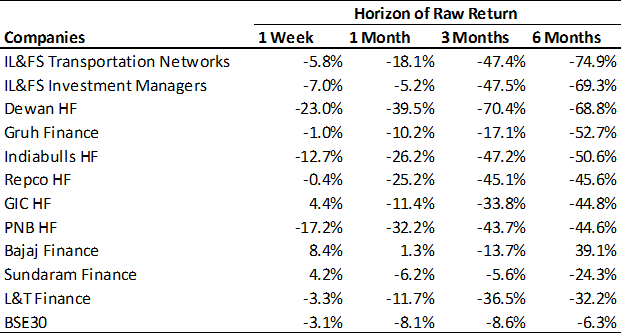

The table below presents the recent share price performance of some of the major NBFC companies. We compute the most recent 1 week, 1 month, 3 months and 6 months raw returns of the NBFC and Housing Finance Companies (HFCs). The highly negative returns in most of these stocks suggest the level of steep correction in the market valuation of the NBFC sector companies, particularly during the last 6 months. As evident from the table, most of the HFC stocks are trading at about half price as compared to 3 to 6 months back. The fall in share prices have been even sharper for two of the IL&FS group affiliated companies – IL&FS Transportation Networks and IL&FS Investment Managers, and Dewan Housing Finance Limited (DHFL), all of which have lost almost three-fourths of their market valuation during the last 6 months. And all three companies have been at the epicenter of the recent NBFC crisis. So, what are the causes of such sharp correction in the market valuation of NBFC stocks? What are the main concerns of the investors in these stocks? This takes us to the next section below.

Table 1: Share Price Performance of Non-Banking Financial Companies (NBFCs), as on 25-Oct-2018.

What Triggered the Panic Reaction in the Market? – Exploring the Causes

A series of defaults led the investors to panic and react the way the stock charts earlier indicated. For example, in mid-September, IL&FS Investment Managers Ltd. (IIML), one of the listed subsidiaries of IL&FS Group, announced that it had defaulted on INR 1,000 Crores loan from Small Industries Development Bank of India (SIDBI), a development financial institution. It had also defaulted on a Letter of Credit (LC) to IDBI Bank and another INR 12,000 Crores of other repayment obligations consisting of both short-term and long-term borrowings. Around the same time, there was news in the market that DSP Mutual Fund was selling the Commercial Papers (CP) of DHFL in the secondary market at a discount to its issue price (or equivalently, at a higher yield).

The market interpreted these announcements as signals of financial distress in the NBFC sector. As a result, most of the NBFC stocks came under severe selling pressure. DHFL tried to alleviate some of these investor concerns by announcing that it had not defaulted on any of its repayment obligations and did not foresee any liquidity issue in servicing their upcoming debt obligations. It thereby hinted that the secondary market sale of the CPs by DSP Mutual Fund were perhaps driven by liquidity needs of the portfolio managers rather than their concerns around the liquidity of the CP issuer. However, as the stock market reactions indicate, the market participants seemed to remain concerned about the financial soundness of these NBFCs.

So, what was it that led the investors to increase their risk aversion for portfolio exposure to these NBFC securities, and revise their valuation expectations sharply downwards? To answer this, we move on to the following sections.

Asset Liability Management in Banks and Financial Institutions – Managing the Mismatch

Banks and Financial Institutions are primarily in the business of borrowing or raising money from investors (shown as liabilities in their balance sheet), and lending them to other borrowers (shown as assets in their balance sheet). The assets (money lent) generate an interest income, while the liabilities (money borrowed) incur an interest expense. For profitable operations, these financial institutions must ensure that the average borrowing rate (cost of funding) must be lower than the average lending rate. The management of this interest rate spread is an essential component of the asset liability management operations in any bank or financial institution. This interest rate spread is often measured by the Net Interest Margin (NIM), defined as the interest income earned on the assets minus the interest expense incurred on the liabilities, divided by the interest-earning assets, and is one of the most important valuation drivers for the financial institutions.

Financial institutions actively monitor and manage this interest rate spread by optimizing the mix of assets and liabilities in their balance sheets. This involves deciding on the nature of assets and liabilities in terms of the following:

(a) Type of interest rates – fixed or floating

(b) Type of depositors and borrowers – retail or wholesale

(c) Type of maturity – money market (short-term) or capital market (long-term) and

(d) Type of denomination – domestic currency or foreign currency.

Asset Liability Management (ALM) involves managing the risks borne by these financial institutions due to mismatch between the nature of these assets and liabilities such as those just mentioned above. This includes interest rate risk (due to mismatch in nature of interest rates), liquidity risk (due to mismatch in nature of maturity profiles) and foreign currency risk (due to mismatch in nature of denominations). In the next section, we specifically focus on funding liquidity risk – the risk of inability of a firm to meet its current or short-term cash flow obligations, which is at the heart of the NBFC liquidity crisis story.

Funding Long-Term Assets with Short-Term Liabilities – Risks and Rewards

The recent NBFC liquidity crisis is primarily an off-shoot of asset liability mismatch in the balance sheets of NBFCs, as the financial institutions were relying heavily on short-term financing for funding their long-term assets. As a result, the amount of deposits and borrowings falling in short-term buckets (which were approaching their redemption dates in near-term) far exceeded the amount of repayments to be received from the loans in the same buckets. Given adequate liquidity in the money market, it can be advantageous for NBFCs to finance their long-term assets with short-term borrowings when the yield curve is upward sloping, as NBFCs can borrow at cheaper, short-term borrowing rates and invest their funds in higher, longer-term assets. This allows the NBFCs to increase their Net Interest Margins (NIMs), and earn higher profits with the same invested capital. However, such a strategy is also exposed to significant refinancing or roll-over risk, as short-term interest rates may fluctuate widely in the event of any illiquidity induced market disruptions.

Hence, when the subsidiaries of IL&FS Group announced a series of defaults on their short-term repayment obligations, and the news of mutual fund managers selling the Commercial Papers of DHFL at a discount in the secondary market became public, the market participants interpreted this information as a signal of impending financial distress for the NBFCs, and immediately became more risk averse in terms of their portfolio exposure to both debt as well as equity securities issued by the NBFCs. This increased risk aversion effectively meant that investors were now willing to pay lower prices for same NBFC securities than their prevailing prices, thereby increasing both the short-term rates in the money market, and the cost of funds of NBFCs, and adversely impacting the NIMs or profitability of NBFCs, as well as their equity valuation.

Over-dependency on Commercial Papers and Credit Rating Downgrades – Going Into a Tailspin

NBFCs were heavily dependent on the issuance of Commercial Papers for funding their long-term assets. Commercial Papers are privately placed, unsecured, short-term money-market instruments issued by highly rated corporate borrowers such as large manufacturing companies, leasing companies and financial institutions. Issuance of Commercial Papers require a minimum credit rating of A3, and have a maturity period that is typically between 7 days and 1 year. Since the yields on commercial papers were lower than the benchmark lending rates, it was beneficial for the NBFCs to borrow from the bond markets rather than the banks. On the other hand, many banks and mutual fund managers also preferred to invest their surplus funds in the money markets rather than government securities as the yields on the Commercial Papers were higher than the reverse repo rates.

However, it is risky and an ill-advised strategy to depend on short-term borrowings such as Commercial Papers as a permanent source of capital as money markets tend to be seasonal in nature, and can be susceptible to rapid tightening in the event of any adverse financial outcome. Therefore, when the subsidiaries of IL&FS Group failed to repay obligations worth INR 12,000 Crores in short and long-term borrowings, one of the Credit Rating Agencies (ICRA) downgraded the credit rating of the borrower from A1+ to Default, citing the liquidity pressure on IL&FS due to its upcoming repayment obligations. This triggered a panic reaction in the capital market, as IL&FS Group is a huge borrower, with an aggregated outstanding debt of INR 91,000 Crores, out of which more than INR 16,000 Crores were of short-term nature. The aggregate borrowings of IL&FS Group accounts for almost 2% of outstanding Commercial Papers in the money market, around 1% of Non-Convertible Debentures (NCDs) and roughly 0.7% of the entire banking system loans. Hence, any significant financial distress to IL&FS Group naturally poses a major systemic risk to the overall banking and financial system in India.

Moreover, as the Indian banks are already burdened with sizable proportion of Non-Performing Assets (NPA) in their balance sheets, they became reluctant in increasing their exposure to the NBFC sector, either through money market instruments or through direct lending. Money market mutual funds also came under heavy redemption pressure, as retail investors became more risk averse, given the significant exposure of mutual funds to IL&FS Group in particular, and NBFCs as a whole. Thus, the rapid deterioration in the credit rating of IL&FS Group led to a general loss of investor confidence in the creditworthiness as well as asset quality of the NBFCs, and a heightened risk aversion towards portfolio exposure to NBFC securities. This further tightened the money market, leading to sharp increase in the cost of borrowings of NBFCs. To make things worse, the rupee was depreciating heavily against dollar due to rapid rise in crude oil prices in the international markets and widening current account deficit. Hence, the interventions made by Reserve Bank of India (RBI) to stabilize the foreign exchange rate through open market operations were creating further liquidity pressures in the market.

Path to Redemption – In Search of Short-term Liquidity and Long-term Planning

Given the immediate liquidity distress, NBFCs are actively exploring various alternative fund raising opportunities to meet their immediate, short-term repayment obligations. This includes raising overseas debt (through instruments such as External Commercial Borrowings) and considering sale of stakes or direct sale of assets to banks, private equity funds and other financial institutions. In fact, financial institutions and private equity funds may also find this as an opportunity to selectively pick the good quality assets from the NBFCs at reasonable discounts, given their urgent needs for liquidity. In the current market conditions, NBFCs with strong balance sheet, prudent asset liability management and high asset quality will have a natural advantage in their fund raising activities. On the other hand, NBFCs with significant exposure to infrastructure and real estate projects with uncertain future cash flows will find it challenging to roll-over their short-term repayment obligations at reasonable costs. The Reserve Bank of India (RBI) has already initiated various steps to ease the liquidity conditions for the NBFCs, by increasing the ceiling for bank lending to a single NBFCs from 10% to 15%.

However, this IL&FS liquidity crisis may also serve as an important wake up call for all the participants in the overall shadow banking sector that has witnessed a phenomenal growth in the recent times, thanks partly to the less stringent supervisory rules and easier prudential norms relative to their banking sector peers. It is worth investigating, whether the rapid growth in NBFC assets came as a result of excessive lending to less creditworthy borrowers. The onus also lies with credit rating agencies to revisit some of their traditional ratings standards to include market intelligence and surveillance based inputs rather than solely depend upon historical data and management estimates of project cash flow forecasts for their credit ratings decisions. Finally, it will be important for the government and the Securities Exchange Board of India (SEBI) to initiate regulatory reforms that can address the shortcomings in their corporate governance mechanisms, and assign accountability and responsibility of top management and the board of directors for such hasty infrastructure and real estate investments alongside inadequate risk management practices, as well as the partners of the designated external audit firms for their audit failures in preventing possible misrepresentation of important financial information.

**********