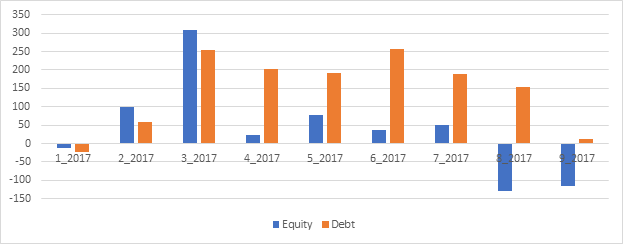

The start-ups in India, as in other parts of the world, are having a dream run over the past four years. The startup India campaign of the Government was able to create a friendly ecosystem that has emboldened young minds to innovate, take risk, raise funds, and flourish. Private equity and venture capital funds are chasing startups that have massively grown in scale, irrespective of whether the idea is really disruptive. During the first quarter of 2018, startups and growth-stage ventures in India, excluding Flipkart and Paytm, have raised more than $2 billion from private equity market (Table 1). Notable among them are Bigbasket ($300 million), Zomato ($200 million), Gaana ($115 million), and Swiggy ($100 million). Tech-based retail raised almost $700 million in past three months, closely followed by Finance (including FinTech).

How many of these companies (Table 1) really have innovative ideas? Well, innovation does not necessarily mean absolutely new and untried inventions. Innovation includes process innovation and in that respect most of the successful startups in India have demonstrated ability to scale up quickly. Gaana, a music streaming platform, has about 60 million subscribers and witnessed a 700% increase in its Internet services accessed by customers in the past one year. Established in August 2014, Swiggy, an online platform that delivers food from restaurants, delivers more than 100,000 orders per day. It has raised more than $255 million in past three years. Lendingkart, an online platform that provides working capital loan to SMEs, which was also incorporated in 2014 had reported a registered user base of 450,000. It has raised more than $173 million so far. Thus, funds chase those start-ups that chase growth.

Table 1: Funds raised in private equity market (January-March 2018): Select List

| Month | Company/Startup | Amount ($M) | Sector | Lead Fund |

| January | Indiabulls Housing Finance | 154.0 | Housing Finance | Yes Bank |

| Mediplus | 117.6 | Healthcare | Goldman Sachs | |

| Rivigo | 50.0 | Logistics | SAIF Partners | |

| Neogrowth | 46.4 | FinTech | Leapfrog Investments | |

| February | Bigbasket | 300.0 | Retail | Alibaba |

| Zomato | 200.0 | Retail | Alibaba | |

| Swiggy | 100.0 | Retail | Naspers and Meituan Dianping | |

| Lendingkart | 87.0 | FinTech | Fullerton Financials | |

| Browserstack | 50.0 | IT | Accel | |

| March* | Gaana | 115.0 | Entertainment | Tencent |

| Grofers | 61.3 | Retail | SoftBank | |

| Chargebee | 18.0 | FinTech | Insight Venture Partners | |

| TOTAL | 1299.30 |

* Up to 26 March 2018

Source: Tracxn and Internet

Start-up valuation is quite challenging and it is more an art than a science. Traditional valuation methods may not apply in most cases. The life cycle of funding of a start-up includes bootstrapping, grants, angel investments, venture capital (VC) funds and private equity (PE). Thereafter, any start-up will have to raise public equity. Of course, venture debt is now available to start-ups, which have already accessed venture fund. Banks would normally avoid financing a startup due to uncertainty and lack of collaterals. Valuation of any start-up, therefore, would depend on the stage of financing life cycle. Valuation method at grant stage would be quite crude and even at angel stage financing happens mainly on the strength of the team and the idea. Sophisticated valuation methods are used when institutional funding (e.g. VC and PE) is accessed by any start-up. Valuation methods used by a PE are similar to the ones used for IPOs (Initial Public Offer).

Therefore, I will try to cover various methods of valuation of start-ups from idea stage to public listing. The multi-part essay will discuss various valuation techniques applicable for start-ups. This article looks at valuation of ideas.

Valuing Idea

How do you value an idea that does not even have a prototype or proof of concept? It is impossible to value an idea that does not have a minimum viable product (MVP)and hence no one would like to fund such an idea. Ideas may come easily if one has keen observation power. However, idea does not fetch money. One needs a committed operator to give shape to an idea that is eventually accepted by the market. Such an operator is called an entrepreneur. An entrepreneur has to get the prototype made with own (including family) money and secure customer validation. Making prototype (proof of concept) is no more costly in India with availability of affordable infrastructure. For example, entrepreneurship development centres in colleges/universities, fabrication labs in technical universities, and incubators supported by the Department of Science and Technology (DST) and Atal Innovation Mission (AIM), Government of India. These institutions or facilities are willing to provide small financial support sufficient to make a few prototypes for testing purposes.

The most important questions in any valuation exercise are (a) who are your customers? (b) how much is the market opportunity? and (c) how much market share one can capture? If a start-up does not have MVP, answering these questions would be almost impossible. Answering the first question (know your customer) is not always easy. On many occasions the beneficiaries may not be the ones who would pay. Famous examples would include Google and Facebook. Google and Facebook control almost 70% of the digital advertisement market. However the majority of the registered users/subscribers of these two Internet giants do not pay for the services. So, Google’s revenue will be driven more by the growth in digital advertisement spending and less by the linear growth in search engine hits.

Idea needs to be priced. Lot of it would depend on the quality of the innovator and her team. The problem with any innovator is in many situations, the inventor may have no clue about the MVP and hence price. In order to get close to the stage of pricing, ideas must be given shape in terms of proof of concept or prototypes.

Even for an established company, which has been into business for many years, pricing a new product or solution is difficult. Take the case of a tractor company that has in its stable an army of tractors of different capacities with maximum engine strength of 32HP (horse power). The tractor company now wishes to launch a new generation of tractors (Generation Y tractors) of 64HP. What should be the price of this proposed high-powered tractor? How much will be the business volume? Will it cannibalize business of its existing tractors? The company had never had such a tractor nor did any other company in India. So there is no compatible data available. The only way the tractor company may try to estimate the launch price of the tractor and the business volume is through a detailed market research. Such research will involve talking to prospective customers (i.e., farmers), identifying whether such a high-powered tractor is at all necessary and knowing what problem of existing users is the proposed tractor going to solve. The research will also help identify the unique selling propositions (USPs) of the new vehicle and perform a proper quality function deployment (QFD) to design the specifications of the tractor. Such an exercise will also help in arriving at the bill of materials (BOM) cost of production. Next question will be what is the USP of this tractor and whether the prospective customers would be willing to pay the price for each USP. For example, if the noise-level of the proposed tractor would be lower than the existing ones, would a customer be willing to pay any extra price for such a feature? If yes, how much more? Answer to these questions would perhaps give some idea of the extra price that a prospective customer will be willing to pay for the new product. It is a well-known fact that in a competitive market, price of a product is not determined by its cost of production. It rather depends on how much a customer is willing to pay (target price). Estimation of business volume for the new tractor would depend on how many of the respondents would like to migrate to the higher version of the tractor. The entire exercise may take anywhere between 6 and 12 months to obtain three basic input for valuation, i.e., the target price, market potential (size), and sales volume. One would argue that it is still easy to price such a new tractor in view of the fact that the company understands the business and has good track record.

Things get further complicated if one wants to set up a new business. Suppose you want to set up a coffee shop chain in one of the metros of India. You plan to set up five coffee outlets in the city. How will you find out your revenue for the first year? It may appear very easy to estimate revenue of this venture as the nature of the business is well known and customers are clearly identified. Even then it may prove difficult to value such entities. Suppose you obtain annual revenue, floor space of outlets, and number of outlets of your competitors in the same city for the past three years. It may be noted that obtaining these information is extremely difficult. Using available information, one may find out two relevant multiples: (a) revenue per outlet, and (b) revenue per square foot. Can the proposed new outlets use these multiple to estimate its first year revenue? If the average annual revenue per outlet of the comparable firms is Rs. 10 million, can the new entity estimate its first year revenue as Rs. 50 million for the five outlets together? The answer is a clear no. Expected revenue per outlet of the new business would depend on the location of the outlet. If an outlet is located in central business district (CBD), average footfall will be higher, but for a limited number of hours. Similarly, if another outlet were set up in a shopping mall, it would expect more customers than one in a residential area. However, the final decision about location of outlets will depend not only on the expected revenue from that area but also on the cost of renting that space. Though an outlet in a shopping mall will enhance the probability of higher daily revenue, the cost will also be higher. The unit economics may show that it would be prudent to set up the coffee outlets in a residential area where the contribution margin could be higher even with a lesser volume. Another advantage of having a coffee shop in a residential locality is long hours of moderate business. Such predictable daily business volume would help the outlet utilize its capacity and staff better. Therefore, the new entrepreneur will have to first decide about the location of the outlets before estimating daily business volume. Next issue that the entrepreneur will face is visibility. How to get the first customer into a new coffee outlet? Customer acquisition cost is quite stiff in such business and the entrepreneur may have to spend a sizable amount in initial years for promotion of its business to get the desired business volume. Interestingly, if the outlet is in the CBD or a shopping mall, a minimum business volume will be assured with no or moderate promotion. Therefore, it may be prudent for the entrepreneur to diversify the location of the proposed five coffee outlets to CBD, shopping mall and residential areas to maximize business volume.

The third example is a tricky one. This is an absolutely innovative business with no parallel. Suppose you have invented a portable brain-imaging machine that can do 50% of the job of a brain scanner at a much lower cost. The imaging machine uses Bluetooth technology to send image of a brain to a nearby hospital within a radius of 2 km. Such image will provide input sufficient for a neurologist to understand possible damage caused to the brain. Consider a road accident where a person having head injury with no external marks on the body was not immediately attended by the rescue team and normally sent home. Later the person may experience severe pain in the brain and develop symptoms of brain damage (e.g., vomiting, fainting). When that person was finally taken to the hospital, he (she) may have lost life due to delay in treatment. The proposed brain-imaging device may save such patients. No one would disagree that it is a socially desirable business proposition and hence should be supported. Who will be the paying customer- the patient or a hospital or an insurance company? Patient will definitely not be a customer. A hospital will not have any incentive to buy such a device as it would have already invested in brain scanner, MRI machine, and other sophisticated devices. The insurance companies may be interested in such a product to minimize compensation claims on avoidable deaths. Therefore sometimes understanding who is your customer is a vital question and that will determine the potential revenue of the start-up. Should the founder therefore follow-up with the insurance companies with the MVP? Another related question would be on the business model. Is this a product or service business? Should the founders sell product or brain images? This is a vital question and the revenue estimation and fund requirement would depend on the business model. If it were a product business, revenue would be higher with associated problems of inventory management, logistics and distribution. If it is a service business, revenue would depend on usage of the device and upfront investment would be higher with longer gestation period for recovery of investment. The pay-for-service model would require additional investment in data storage and processing. The problem with valuing such ideas is that there is no comparable. The proposed device cannot be compared with a scanner and hence its business volume. Scanner would be far more efficient and hence costly. Also, the proposed imaging devise is not a substitute for the scanner. Therefore, estimating the market potential and revenue of such devices using brain scanner, as benchmark would be extremely risky. Another problem with any medical device is that it needs certification of appropriate authority before it can be administered on any patient. Such certification in turn would depend on the use-cases. Therefore, the inventor of such a device would need to make dozens of prototypes and get some hospitals/ ambulance services use it for evaluating its efficacy. No one would talk about revenue till the idea is converted into an acceptable product that has got ‘satisfactory’ certificate from users.

The above examples highlight that it would be futile to try to value any new idea without an MVP. What is required at the stage of idea is to evaluate (a) what is unique in the idea? (b) is it possible to get a viable product from the idea; (c) how much investment would be required to get the first ten customers? It is only then one can think about valuing an idea. So, a winning idea will be funded on the strength of the team and how quickly it can be taken to the market. No valuation is necessary at this stage.

The next part will discuss valuation of pre-revenue companies.